You look out at a noisy world with many paths ahead of you. Which way do you go? How do you sort out conflicting information? We believe that the right way to navigate the chaos is to hire an investment advisor who works as your legal fiduciary. Where your needs and interests are contractually bound to come first. Our commitment to the fiduciary standard is core to our values and guides our every action. Whether you are starting out, raising a family, or enjoying your retirement, our wealth advisors in Denver will guide you along your unique path to financial freedom. Our goal is to help you grow in your sense of financial freedom. To enjoy life, build rich relationships, and pursue your passions.

Talk to an AdvisorGo to Talk to an Advisor by clicking here

At GreenStar, our goal is to help you reach your goals. We do this by transforming your goals into an actionable strategy that is simple, proactive, and accountable. We deliver truly comprehensive financial advice and a variety of services that grow, change, and scale as your life progresses. Our core services are:

Your holistic investment and Wealth Management in Centennial should be as unique as you and created for you.

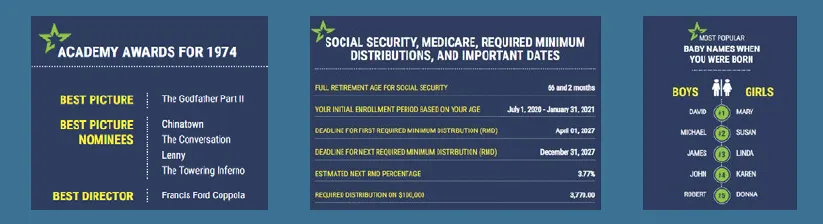

What were the most popular baby names? What day of the week was it? How much was a loaf of bread?

At GreenStar, we believe that when you are informed you are empowered. For us this means offering educational resources that are clear, interesting, and readily accessible.

If you are searching for one of the most reliable and reputed financial advisors in Centennial, you can choose GreenStar. We offer the right advice, guidance, and support to achieve the much-needed financial freedom. You can approach us for a wide range of services, including financial planning, estate planning, risk management, fiduciary financial advice, and much more.

Your search for the right financial advisors in Centennial easily ends with us. Our method of approach is comprehensive and addresses the core issues to help accomplish the expected goals in life. Our Centennial wealth management team contains vastly experienced and skilled financial experts who are highly knowledgeable.

We follow ethical practices and build long lasting relationships with our clients. GreenStar leaves nothing to guesswork when it comes to developing a systematic and actionable plan. We work as your trusted companion to fulfill your needs. Please feel free to contact us to know more about our wealth advisor services in Denver, Centennial.